competitiveness and attractiveness

NAVAL INDUSTRY IN A PRECARIOUS POSITION OVER THE NEXT 3 YEARS CALLS FOR BOLD GOVERNMENT MEASURES

dec. 2022

Download the position paper

The GICAN represents the French naval industry, a robust sector comprising 650 companies, with a turnover of 13 billion euros in 2021 and more than 50 000 direct jobs. Shipyards, systems integrators, equipment manufacturers, subcontractors, and design offices work together to design, build and maintain civil and military vessels, submarines, and maritime drones (both underwater and surface). They also leverage their expertise to provide solutions in the field of renewable marine energy (such as offshore wind farm substations and tidal turbines). They contribute to France’s sovereignty by developing solutions to monitor and defend territorial waters and project forces into crises zones, while also providing the vessels essential for maritime logistics and energy supply solutions.

a long-cycle industry in a precarious position

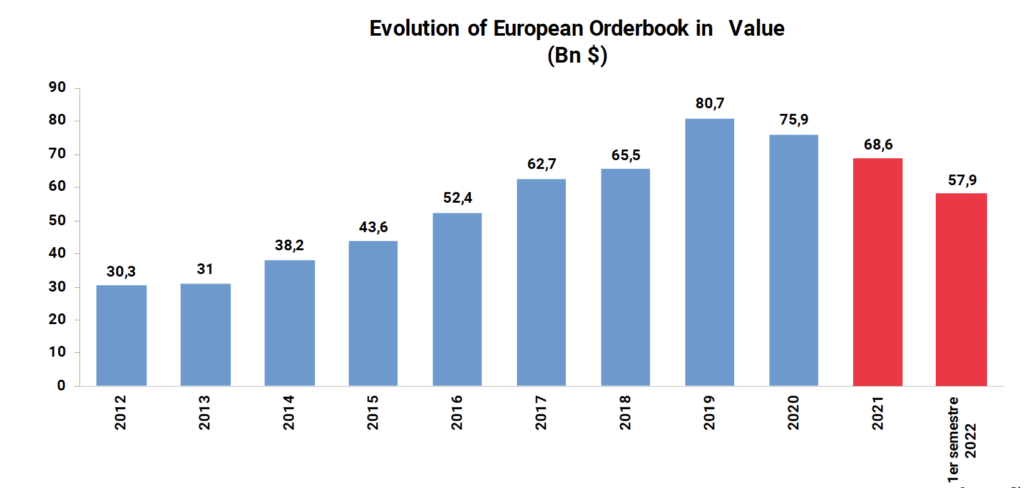

Although turnover figures have shown a degree of growth in recent years and strong resilience during COVID-19, it must be acknowledged that the situation is precarious. As a long-cycle industry, the naval sector is currently delivering vessels that were ordered several years ago. However, the order books of French shipyards and European yards more generally are in decline, both in absolute and relative terms to Asian competitors (China and South Korea) and Turkey.

A decline in European order books

the decline in activity will impact employment and creat recruitment challenges

-The downturn in activity over the next three years will have a major impact on employment, leading to subsequent difficulties in hiring new staff during a recovery for two primary reasons:

-A loss of confidence in a sector perceived to be in decline (an image the industry has struggled with since the 1980’s crisis).

-A shortage of human ressources, as several other sectors (aerospace, nuclear) require similar high-levem skill sets.

Following the COVID-19 crisis, Europe has been the hardest hit by the fall in orders.

why is the french naval industry unable to grow its order book ?

The lack of productivity in the French naval industry : Beyond the issues common to many French industries (the need to reduce production taxes, which are much higher than in other European countries), the naval industry faces several specific factors that create a productivity deficit :

Several countries are known to support and subsidize their naval industries in absolute breach of WTO agreements. Europe remains the only continent to strictly apply international law. However, no retaliatory measures are taken against this distortion of competition. This has a disproportionate impact on European yards because ships are not classified as imported goods; consequently, they are not subject to import duties and do not benefit from standard WTO trade defense instruments.

Raw Material Costs and Supply European steel and aluminum are more expensive than those found on other continents. Yet raw materials can account for a significant proportion f a vessel’s price (up to 60% for smaller ships). Current supply chain issues further complicated matters for shipyards, which face late-delivery penalties. The introduction of the Carbon Border Adjustment Mechanism (CBAM) will further increase raw material costs for importing manufacturers, creating an even wider price gap for the finished product compared to Asian shipyards. The system also tends to encourage the importation of hull sections and bare hulls for outside the EU (Turkey, Morocco, etc) reducing the value-added produced in France and Europe.

The lack of domestic human resources for certain trades forces manufacturers to rely on posted workers. Contrary to popular belief, this reliance actually entails higher costs for the company.

European shipowners prefer to purchase their vessels in Asia rather than in Europe, fostering the emergence of ultra-competitive industrial giants, particularly as these are heavily state supported.

The risk of French shipyards disappearing altogether can not be ruled out. This would have a major impact on the entire supply chain and on European sovereignty.

While equipment manufacturers do export, they are increasingly subject to local content requirements in many of the countries where they operate, meaning the value-added is no longer produced in France.

The state must therefore act to ensure our industry remains competitive and strong internationally.

key instruments to be implanted rapidly in france :

#Point A

Recognition of unfair competition and the implementation of measure to combat it.

#Point B

Improving French competitiveness by reducing production taxes, simplifying the use of posted workers, and ensuring the Direction Générale du Travail understands the sector’s challenges, in exchange for industry commitments to training in high-demand trades.

#Point C

Supporting innovation and decarbonization, the only way for France to position itself as a leader in green maritime transport. This includes simplifying access to France 2030 funds for R&D and industrialization via state agencies (ADEME, BPI France, etc..). Innovation must not only be supported but its deployment and industrialization must be actively encouraged.

#Point D

The creation of a support found for vessels greening and the first commercial applications of new technologies, with resources allocated to shipyards and equipment manufacturers. It is vital to offset the additional costs associated with installing decarbonization equipment. Like the automative and aerospace sectors, the naval industry requires its own dedicated recovery and greening fund.